Why do countries need industrial policy?

The case for looking beyond market failures

For much of the late twentieth century, industrial policy carried the whiff of failure. The dominant orthodoxy held that governments should set the rules and then step aside, leaving markets to allocate capital and pick the winners that deserved to win. To advocate for the state to actively steer the economy towards particular firms or sectors was, in polite economic company, faintly embarrassing. Yet since the 2010s, industrial policy has come roaring back into fashion. Confronted with climate change, fragile supply chains, and geopolitical rivalries, governments have rediscovered the appeal of an activist state. The question is no longer whether governments should pursue industrial policy, but what kind.

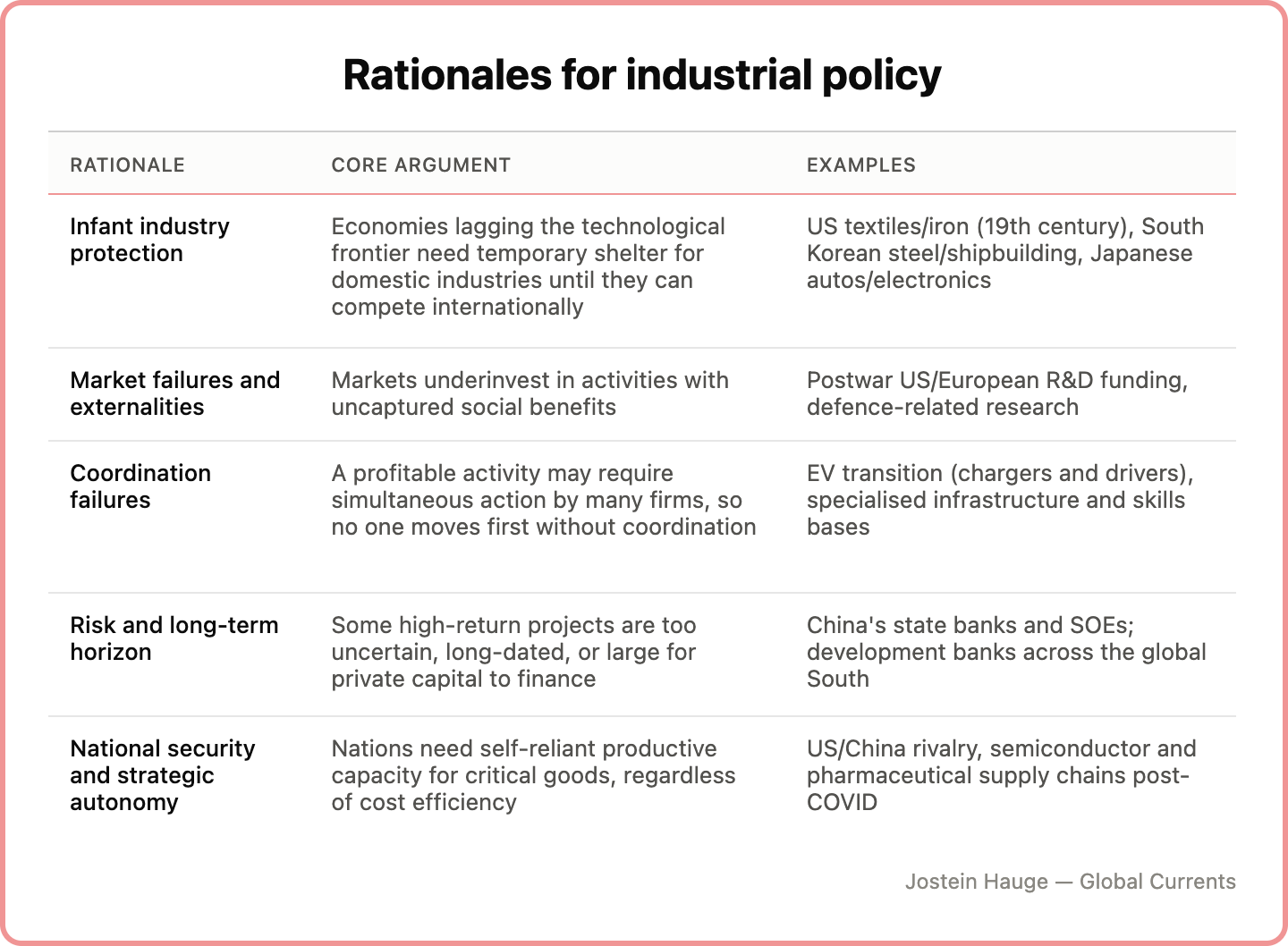

Yet even as the practice has been rehabilitated, the way many people think about it is surprisingly narrow. Ask a government economist to justify a particular intervention, and the answer will often be framed through the language of market failures. Where is the externality the policy is meant to correct? This lens is not wrong, and I will give it its due. But it is not comprehensive enough. It treats industrial policy as a series of narrow technical patches applied to an otherwise well-functioning market, obscuring the deeper and older reasons why states have always intervened. My aim with this essay is twofold: to set out the full range of rationales behind industrial policy, older and newer, and to show that the market-failure lens captures only a fraction of why countries need it. Some are widely understood; others, particularly those concerning national security, have been transformed by recent events and deserve to be brought up to date. The table below summarises the full set of rationales.

Before turning to those rationales, an honest concession is in order. Industrial policy can fail, it has failed, and it will fail again. The case for it is not a starry-eyed faith in the state as an omniscient force that always chooses correctly. Governments are prone to failure, corruption, and rent-seeking. But without a government that steers the market in the right direction, it is practically impossible to transform an economy from low income to high income, or to push it towards more innovative, high-value activities. Industrial policy can fail, yes, but without any industrial policy, failure is a certainty. Every country that has built up strong productive capabilities has used industrial policy in some form.

The infant industry argument

The earliest rationale for industrial policy, and arguably the most important for developing countries, is the infant industry argument. First articulated by Alexander Hamilton, it postulates that an economy lagging behind the global technological frontier — as the United States was in the late eighteenth century — needs to protect and nurture its industries in their infancy until they can compete internationally. The German political economist Friedrich List later supplied the theoretical framework in his National System of Political Economy, arguing that infant industries could not develop without a strong, supportive government, and that the state had a duty to promote activities that increase national wealth and power, even where that meant jumping ahead of a country’s current comparative advantage.

The strategy has a strong track record among the world's most successful industrializers, beginning with the United States itself, the birthplace of the argument. The US used steep tariffs throughout the nineteenth century to nurture its manufacturing base, protecting industries like textiles and iron from more advanced British competitors until they could stand on their own. South Korea followed a similar path in the 1960s and 1970s, shielding its steel and shipbuilding industries, helping transform a war-torn economy into an industrial powerhouse. Japan protected its automobile and electronics sectors from foreign competition in the postwar decades, giving firms like Toyota and Sony room to mature and refine their technology before facing international rivals. In each case, temporary protection gave domestic firms the breathing room to build capacity and expertise that they could not have developed if directly exposed to established foreign competitors in a nascent stage of their development.

Market failures and externalities

In contemporary discussions, the case for industrial policy is most often framed in the language of market failures. When a government department proposes an intervention, treasuries and departments of finance routinely demand that it identify the specific market failure the policy is meant to correct. The concept emerged from the neoclassical school — above all through the work of Arthur Cecil Pigou — and acknowledges that markets sometimes produce suboptimal outcomes, in tension with the tenet that, all else equal, markets deliver the most efficient results.

The classic market failure is an externality: a consequence of commercial activity that affects third parties without being reflected in prices. Environmental damage is the standard negative example, but positive externalities matter more here, the textbook cases being R&D and worker training. Firms underinvest in both from society’s point of view. Some technological knowledge cannot be patented, and workers carry their skills to new employers, so the firm that trained them does not capture the full return. The lack of private research investment after World War II was the principal reason European and American governments funded R&D directly, and state-funded research, much of it defence-related, is widely credited with making the United States’ innovation system world-leading.

Coordination failures and public inputs

The market-failure story takes for granted a market that already exists and merely misfires at the edges. The rationales for industrial policy that follow from here are harder to squeeze into that frame. The first is coordination failure. Even where no externality exists, a desirable activity may be profitable for a single firm only if many others act at the same time. An upstream supplier will not build a components plant until assemblers exist to buy from it, and assemblers will not commit until suppliers and a trained workforce are in place. Nobody moves first, and the economy settles into a low-level equilibrium worse for everyone.

This problem is the basis for the “big push” argument, developed by Paul Rosenstein-Rodan. His core idea was that a large, coordinated wave of investment across many industries at once could be self-sustaining in a way that piecemeal, isolated investments would not. The electric-vehicle transition is a good illustration. Drivers will not switch without a charging network, and the network will not be built without drivers. Markets can remain stuck not because prices are wrong but because no actor can profitably go first. A related strand concerns activity-specific public inputs — specialised infrastructure, regulatory regimes, or skills bases that no single firm will supply but on which a whole sector relies. Both broaden the case for intervention well beyond the patching of isolated externalities.

Risk and the long-term horizon

A further rationale for industrial policy concerns risk. Some industrial projects carry returns that are high for society but too uncertain, too long-dated, or too large for private investors to shoulder alone. Commercial banks want collateral and predictable repayment; venture capital wants an exit within a few years. Neither is well suited to financing a first steel mill or a national semiconductor industry, where the payoff may take decades and failure is a real possibility. The state, with a longer horizon and the capacity to pool risk across ventures, can step in where private finance will not. Historically, this has happened through development banks and state-owned enterprises, both enormously important across the global South, where capital markets willing to bear such risks are especially scarce.

This willingness to absorb risk that private finance won’t touch is one of the central dividing lines between the economic systems of China and the United States. China’s state banks and state-owned enterprises have financed decades of investment in industries deemed vital for economic development but which would have struggled to attract private capital. The state absorbs the early losses and long payback periods that commercial lenders and shareholders are structurally unwilling to bear. The United States, by contrast, has relied overwhelmingly on private capital markets to allocate investment. Those markets are built around quarterly earnings and shareholder returns rather than decade-long industrial buildouts. The result in the United States is a financial system well suited to funding startups with fast exits, but poorly suited to steering investment into long-term projects that serve public needs and national development objectives.

Beyond financing risk, these state-owned institutions carry further benefits that the market-failure framework struggles to price: national security, economic autonomy from multinational capital, and public control over strategic industries and natural resources. This is where I turn next.

National security, resilience, and strategic autonomy

If one rationale has been transformed by recent events, it is this one. National security has always lurked in the background of industrial policy. It is no accident that so much of the research that built the American innovation system was defence-related, or that countries have long guarded their capacity to produce steel, ships, and armaments. But for a generation this was treated as a narrow exception to the free-trade rule, invoked for a handful of obviously military goods and otherwise set aside. That has changed fast. The grounds for intervention have widened from stimulating development, to protecting national security and preserving self-reliance in an openly contested and highly competitive world.

Three shocks have driven this shift. The COVID-19 pandemic exposed how fragile globalised supply chains could be when everyone needed things like masks, medicines, and ventilators at once. The semiconductor shortages that followed showed that a handful of chokepoints — many concentrated in a single geopolitically exposed region — could bring entire industries to a halt. And intensifying economic rivalries between major powers, especially the United States and China, have made national security measures central to economic policymaking.

Crucially, this rationale does not fit the market-failure template at all. The aim is not to correct a mispriced externality but to ensure a nation retains or builds the capacity to produce what it deems critical — semiconductors, pharmaceuticals, batteries — even when the global market would supply them more cheaply from abroad. A country may knowingly accept a less efficient domestic industry as the price of not depending on a strategic rival. It’s a calculation about power and vulnerability, not efficiency. This logic has been central to China’s industrialization, where industrial policy was driven far less by market failures than by the urgency of technological catch-up, national sovereignty, and strategic autonomy.

Beyond market failures

The rationales surveyed here — infant industry protection, market failures, coordination problems, risk-bearing, and national security — do not compete with one another so much as accumulate. A single policy, such as subsidies for a domestic semiconductor industry, might simultaneously nurture a technologically lagging sector, correct underinvestment in R&D, solve a coordination problem between chipmakers and downstream manufacturers, absorb risk no private lender would take on, and secure a supply chain against geopolitical rupture. Reducing this to a single market failure to be patched misses most of what is actually happening. Industrial policy is not a narrow corrective tool bolted onto an otherwise self-sufficient market. It is a recurring feature of how every country implements long-term plans to develop productive capacity.

If industrial policy is understood only as a correction to the market, then its proper domain shrinks to a handful of textbook externalities, and anything beyond that looks like unwarranted state overreach. But if governments recognize the fuller set of rationales, the calculus changes. A country may rationally accept a less efficient domestic industry in exchange for resilience against supply shocks or dependence on a rival power, a trade-off the market-failure framework has no language for. None of this licenses complacency. Industrial policy remains prone to capture, misallocation, and failure, and no rationale here is a guarantee of success. But the choice was never between an interventionist state and a neutral market getting it right on its own. It is between industrial policy done with a clear-eyed view of why it is needed, and industrial policy done blindly.